Fiscal Policy

The government’s policy in regard to taxation and spending programs.

Fiscal policy is the means by which a government adjusts its spending levels and tax rates to monitor and influence a nation’s economy. It is the sister strategy to monetary policy through which a central bank influences a nation’s money supply.

Fiscal policy deals not only with the quantity but the quality of public finance as well i.e how the revenue would be raised and quality of expensiture – productive or wasteful.

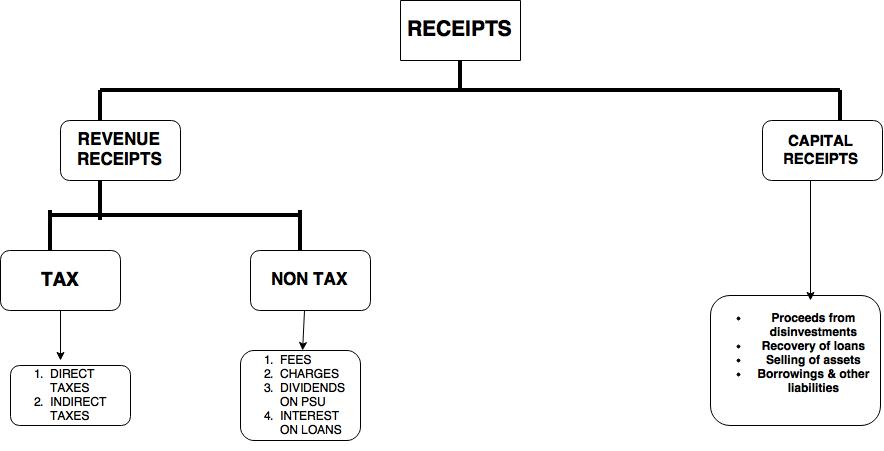

Revenue receipts are recurrent receipts.

Definitions of Deficits

Deficits is the difference between expenditure and receipts. Deficits get collected to form debt.

1. Revenue deficit

= Revenue Expenditure- Revenue Receipt

2. Fiscal Deficit

=Total Expenditure – (Revenue Receipt + Non debt creating capital receipt)

=BORROWINGS

Fiscal deficit is the difference between what the government earns and its total expenditure. That is the difference between what is received by the government on revenue account and all the non-debt creating capital receipts like recovered loans and disinvestment proceeds , and the total expenditure .It amounts to all borrowings of the government in a given period.

High FD on capital account is not worrying because expenditure is on producing income generating assets such as infrastructure.

3. Primary deficit

= Fiscal Deficit – Interest payment

Primary deficit is the difference between the fiscal deficit and the interest payments. It tells us about the current state of government finances and factors out interest burden on loans by previous governments.

The concept helps in assessing the progress of the government in its-fiscal control efforts.

4. Budget deficit

= Total expenditure – Total receipt

Budget deficit considers only the difference between the total budgeted receipts and the expenditure. It was abolished in 1997.

Fiscal Deficit mirrors the health of government finances most accurately unlike the budget deficit concept. BD does not cover all borrowings but only that portion of the borrowings for which government relies on printing money by the RBI

5. Monetised deficit

Monetised deficit is the borrowings made from the RBI through printing fresh currency. It is resorted to when the government can not borrow from the market (banks and financial institutions ) any longer due to pressure on interest rates or for reasons like fresh money injection into the economy is necessary to push growth up.

It corresponds to the budget deficit that is discarded as a concept since 1997. It is discontinued from 2006 as a part of the FRBM 2003.

6. Deficit Financing

Deficit Financing is the phrase used to describe the financing of gap between Government receipts and expenditure. Such gap is called budgetary deficit. it is financed by printing fresh money by the RBI.

7. Effective Revenue Deficit

Effective Revenue deficit is a new term introduced in the Union Budget 2011-12. Effective revenue deficit has been in defined as the difference between the revenue deficit and the grants for creation of capital assets.

If we strip out a portion of revenue expenditure that has been classified as grant for creation of capital assets

Ways & Means Advances (WMAs)

This is an arrangement between government and RBI started on April 1,1997 after abolition of budgetary deficit under which the government borrows from RBI only to meet a temporary mismatch between its revenue and expenditure. These borrowings are on a quarterly basis, so that only after the debt of one quarter (at least 75% of debt) has been payed off by government/ so that it can borrow in next quarter. This mechanism aims at disciplining the government and also providing autonomy to RBIs monetary policy.

FRBM Act 2003

Fiscal Responsibility and Budget Management (FRBM) became an Act in 2003. The objective of the Act is to ensure inter-generational equity in fiscal management, long run macroeconomic stability, better coordination between fiscal and monetary policy, and transparency in fiscal operation of the Government.

The Government notified FRBM rules in July 2004 to specify the annual reduction targets for fiscal indicators.

- The FRBM rule specifies reduction of fiscal deficit to 3% of the GDP by 2008-09 with annual reduction target of 0.3% of GDP per year by the Central government.

- Similarly, revenue deficit has to be reduced by 0.5% of the GDP per year with complete elimination to be achieved by 2008-09.

- It is the responsibility of the government to adhere to these targets. The Finance Minister has to explain the reasons and suggest corrective actions to be taken, in case of breach.

- Further, the Act prohibits borrowing by the government from the Reserve Bank of India, thereby, making monetary policy independent of fiscal policy.

- The Act bans the purchase of primary issues of the Central Government securities by the RBI after 2006, preventing monetization of government deficit.

- The Act also requires the government to lay before the parliament three policy statements in each financial year namely Medium Term Fiscal Policy Statement; Fiscal Policy Strategy Statement and Macroeconomic Framework Policy Statement.

- To impart fiscal discipline at the state level, the Twelfth Finance Commission gave incentives to states through conditional debt restructuring and interest rate relief for introducing Fiscal Responsibility Legislations (FRLs). All the states have implemented their own FRLs.

- The Act binds not only the present government but also the future Government to adhere to the path of fiscal consolidation. The Government can move away from the path of fiscal consolidation only in case of natural calamity, national security and other exceptional grounds which Central Government may specify.

Government of India was on the path of achieving this objective right in time. However, due to the global financial crisis, this was suspended and the fiscal consolidation as mandated in the FRBM Act was put on hold in 2007-08. As a result of fiscal stimulus, the government has moved away from the path of fiscal consolidation.

Amendments to FRBM Act

As per the amendments in 2012, the Central Government has to take appropriate measures to reduce the fiscal deficit, revenue deficit and effective revenue deficit to eliminate the effective revenue deficit by the 31st March, 2015 and thereafter build up adequate effective revenue surplus and also to reach revenue deficit of not more than 2 % of Gross Domestic Product by the 31st March, 2015 and thereafter as may be prescribed by rules made by the Central Government.

Further, the Central Government may entrust the Comptroller and Auditor-General of India to review periodically as required, the compliance of the provisions of FRBM Act and such reviews shall be laid on the table of both Houses of Parliament.

Vide the Finance Act 2015, the target dates for achieving the prescribed rates of effective deficit and fiscal deficit were further extended.

- The effective revenue deficit which had to be eliminated by March 2015 will now need to be eliminated only after 3 years i.e., by March 2018.

- The 3% target of fiscal deficit to be achieved by 2016-17 has now been shifted by one more year to the end of 2017-18.

New Zealand was the first country to enact a Fiscal Responsibility Act in 1994.

Fiscal consolidation

Fiscal Consolidation refers to the policies undertaken by Governments (national and sub-national levels) to reduce their deficits and accumulation of debt stock. FRBM Act is a milestone towards fiscal consolidation path.

Plan and Non Plan Expenditure classification and its unsustainability

Plan expenditure means expenditure for five year plans in India whereas non plan expenditure lies outside plan and for which no provisions can be made in five year plans.

The Fourteenth Finance Commission has formulated its recommendations without any reference to the distinction between Plan and non-Plan outlays. This will facilitate greater attention to maintenance expenditure, and reduce incentives to boost capital works and show large-sized plans.

The Plan mindset should be replaced with a development mindset, of which government budgets are one element, he said.

Subsidy

Part of cost shared by government on essential commodities generally with the aim of promoting economic and social equity.

Merit Subsidy

Subsidies which benefit the society much more than they benefit select individual or group.

Eg. mass immunization, primary education, public utility.

Non merit subsidies

Subsidies which benefit the individual or group much more than they benefit society.

Eg. higher education, petroleum

Explicit Subsidies

There is explicit provision in budget.Eg Food

Implicit Subsidies

No budgetary provision yet goods are available at cheaper rate . Eg higher education.

Crowding Out

When government increases its expenditure either by sourcing through taxes or by loans from banks which leaves less money for private sector to spend. If source is tax then public is left with less surplus and if government source is loans then it increases interest rates making credit costlier for private sector. Effectively excess government expenditure crowd out private investment.

This is in contrast to Crowding In effect.

Public good

Goods which are

- Non rival : consumption by one does not reduce quantity of consumption by others

- Non excludable : once provided everyone can use it

Giffen good

A good for which demand increases as the price increases, and falls when the price decreases. A Giffen good has an upward-sloping demand curve, which is contrary to the fundamental law of demand which states that quantity demanded for a product falls as the price increases, resulting in a downward slope for the demand curve.

A giffen good occurs when a rise in price causes higher demand because the income effect outweighs the substitution effect.

Suppose you have a very low income and eat two basic food stuffs rice and meat. Meat is a luxury and is much more expensive than rice. If rice increased in price, your disposable income is effectively reduced significantly therefore, you buy less meat, to compensate for less meat you buy more rice to gain enough calories.

It is quite rare and whether it really happens has a little uncertainty. But, it shows that there are two factors affecting demand price (substitution effect) and income.

Veblen Good

A good for which demand increases as the price increases, because of its exclusive nature and appeal as a status symbol. A Veblen good, like a Giffen good, has an upward-sloping demand curve, which runs counter to the typical downward-sloping curve. However, a Veblen good is generally a high-quality, coveted product, in contrast to a Giffen good which is an inferior product that does not have easily available substitutes. As well, the increase in demand for a Veblen good reflects consumer tastes and preferences, unlike a Giffen good, where higher demand is directly attributable to the price increase.

Twin deficits

Fiscal deficit and Current account deficit is together called as Twin deficits.

Nicely done

LikeLike