AGRICULTURE

- The agriculture sector registered an annual growth of 3.8 per cent in value added in the decade since 2004-05 on the back of increase in real prices (31 per cent during 2004-05 to 2011-12).

- The committee set up by the Ministry of Agriculture under the chairmanship of S. Mahendra Dev to come up with updated methodology to compute terms of trade between agriculture and non- agriculture has observed that, during 2004-05 and 2013-14, terms of trade have become favourable for agriculture.

- A strategy of price-led growth in agriculture is, therefore, not sustainable due to a rise in high level of food inflation, seasonal and short- term price spikes in some commodities like onions, tomatoes, and potatoes.

- The room for increasing production through raising cropped area is virtually non-existent.

- Hence the strategy for growth in agriculture has to rely more on non-price factors, viz., yield and productivity.

OVERVIEW OF THE AGRICULTURAL SECTOR

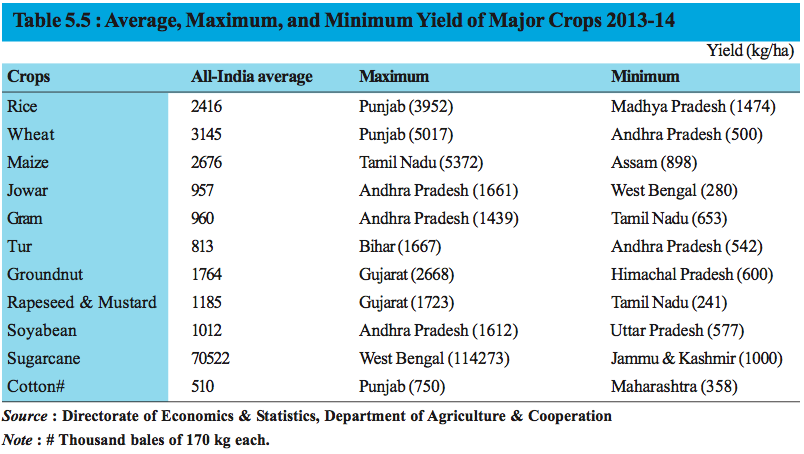

AREA, PRODUCTION, AND YIELD

As compared to last year’s production of 265.57 million tonnes, current year’s production of foodgrains is lower by 8.5 million tonnes i.e 257.07 million tonnes. This decline has occurred on account of lower production of rice, coarse, cereals and pulses due to erratic rainfall conditions during the monsoon season-2014.

To improve resilience of the agricultural sector and bolster food security—including availability and affordable access—our strategy for agriculture has to focus on improving yield and productivity.

An inverse relationship is noticed between increase in yield over time and the average cost of production of various crops in real terms. This clearly points towards the fact that productivity increases, especially in low productivity states/regions, can significantly contribute towards reducing cost-push food inflation.

Yield is contingent upon several factors like variety and quality of seeds, soil quality, irrigation – including quality of water—fertilizers— including their proportion—pesticides, labour, and extension services. Prices received by farmers and the certainty or assurance of getting a particular price also incentivize farmers to take to a particular crop and use quality inputs in its cultivation. The status of some of these factors in India is described in the following paragraphs.

DRIVERS OF GROWTH

Agricultural Research and Education

The Indian Council of Agricultural Research (ICAR) is engaged in developing new crop varieties with specific traits that improve yield and nutritional quality along with tolerance / resistance to various biotic and abiotic stresses.

The paradigm shift in yield/productivity required for the second green revolution can be achieved, with greater outlay on basic research by creating research institutions on the pattern of Indian Institutes of Technology (IIT) and Indian Institutes of Sciences (IIS). It is imperative to make Indian agricultural growth science-led by shedding ‘technology fatigue’. Budget 2014-15 provided for the establishment of two institutes of excellence in Assam and Jharkhand with an initial sum of Rs 100 crore.

Agricultural Extension

To ensure last-mile connectivity, extension services need to be geared up to address emerging technological and information needs.

- The NSSO 70th round survey indicates that about 59 per cent of farmers do not get much technical assistance and know-how from government-funded farm research institutes or extension services.

- Effectiveness of the lab-to-farm programme can be improved by leveraging information technology and e- and mobile (m-) applications, participation of professional NGOs, etc.

- The Budget 2014-15 allocation of Rs 100 crore to Kisan TV for disseminating real- time information to farmers regarding new farming techniques, water conservation, organic farming, etc. will partly make up for the existing adverse ratio of one extension worker for every 800 to 1000 farmers and provide farmers a direct interface with agricultural experts.

Irrigation

Indian agriculture is still heavily rainfall dependent with just 35 per cent of total arable area being irrigated, and distribution of irrigation across states is highly skewed.

The wide gap between gross cropped area and gross irrigated area which has not improved much since the First Five Year Plan period needs to be bridged for increasing productivity, production, and resilience .

- Accelerated Irrigation Benefit Programme (AIBP) ,1996-97 : for the completion of incomplete irrigation schemes ; 85.03 lakh ha irrigation potential created under the AIBP

- The Command Area Development Programme : has also been amalgamated with the AIBP: the gap between irrigation potential that has been created and that is utilized.

- National Water Grid for transferring water from water surplus to water deficit areas have been made from time to time.

- Focus on micro-irrigation systems like drips and sprinklers would significantly increase water-use efficiency and productivity.

Seeds

It is estimated that the quality of seed accounts for 20-25 per cent of agricultural productivity.

- During 2014-15, there has been shortfall in the availability of certified/quality gram, lentil, pea, soyabean, and potato seeds.

- Given our import dependence on oils and pulses and susceptibility of potato to inflation, steps are necessary to avoid shortages of certified seeds of these commodities.

Fertilizers

The following major initiatives were taken in the fertilizer policy of the government in 2014- 15:

- Notification of the Modified New Pricing Scheme (NPS-III) for existing urea units on 2 April 2014 in order to address the issue of under- recoveries of the existing urea units on account of freezing of fixed cost at the 2002-03 level. The modified policy has been implemented for a period of one year from the date of notification.

- Further, the government had notified the New Investment Policy 2012 on 2 January 2013 to facilitate fresh investment in the urea sector to make India self-sufficient. The amendment to New Investment Policy – 2012 has been notified by the Department of Fertilizers on 7 October 2014.

- As against the targets for domestic production of 89.68 lakh tonnes and 33.51 lakh tonnes for nitrogen and phosphate for April-November 2014,actual production was 82.86 lakh tonnes and 25.05 lakh tonnes respectively.

Credit

The following measures have been taken for improving agricultural credit flow and bringing down the rate of interest on farm loans:

- Agricultural credit flow target for 2013-14 was fixed at Rs 7,00,000 crore and achievement was Rs 7,30,765 crore (Provisional), as against Rs 6,07,375 crore in 2012-13. Agricultural credit flow target for 2014-15 has been fixed at Rs 8,00,000 crore against which achievement has been Rs 3,70,828.60 crore (Provisional) up to 30 September, 2014.

- Farmers have been availing of crop loans up to a principal amount of Rs 3,00,000 at 7 per cent rate of interest. The effective rate of interest for farmers who promptly repay their loans is 4 per cent per annum during 2014-15.

- In order to discourage distress sale of crops by farmers, the benefit of interest subvention has been made available to small and marginal farmers having Kisan Credit Cards for a further period of up to six months (post- harvest) against negotiable warehouse receipts (NWRs) at the same rate as available to crop loan. Other farmers have been granted post-harvest loans against NWRs at the commercial rates.

- From 2014-15, in order to provide relief to farmers on occurrence of natural calamities, interest subvention of 2 per cent will continued to be available to banks for the first year on the restructured loan amount on account of natural calamities and such restructured loans will attract normal rate of interest from the second year onwards as per the policy laid down by RBI.

- The Interest Subvention Scheme for short- term production credit (crop loans) which was started by the Government of India in 2006-07 was extended to private-sector banks from 2013- 14.

- Presently the total number of loan accounts stands at 5.72 crore.

- RBI and National Bank for Agriculture and Rural Development (NABARD) study indicate that the crop loans are not reaching intended beneficiaries and there are no systems and procedures in place at several bank branches to monitor the end-use of funds.

- Although overall credit flow to the agriculture sector has increased over the years, the share of long-term credit in agriculture or investment credit declined from 55 per cent in 2006-07 to 39 per cent in 2011-12.

- As much as 40 per cent of the finances of farmers still comes from informal sources.

- Usurious moneylenders account for a 26 per cent share of total agricultural credit.

Inadequate targeting of beneficiaries and monitoring/supervision of the end-use of short- term crop loans for which interest subvention scheme is applicable and decline in long-term/ investment credit to agriculture are issues that need to be addressed on priority basis.

Mechanization

Agricultural mechanization increases productivity of land and labour by meeting timeliness of farm operations and increases work output per unit time.

- Although India is one of the top countries in agricultural production, the current level of farm mechanization, which varies across states, averages around 40 per cent as against more than 90 per cent in developed countries.

- Farm mechanization in India has been growing at a rate of less than 5 per cent in the last two decades.

The main challenges to farm mechanization are,

- a highly diverse agriculture with different soil and climatic zones, requiring customized farm machinery and equipment and,

- largely small landholdings with limited resources.

- Credit flow for farm mechanization is less than 3 per cent of the total credit flow to the agriculture sector.

A dedicated Sub-Mission on Agricultural Mechanization has been initiated in the Twelfth Plan, with focus on spreading farm mechanization to small and marginal farmers and regions that have low farm power availability.

GCF in Agriculture and Allied Sectors

The GCF in agriculture and allied sectors relative to agri-GDP in this sector has shown an improvement from 13.5 per cent in 2004-05 to 21.2 per cent in 2012-13 at 2004-05 prices .

MAJOR SCHEMES OF THE GOVERNMENT

Rahtriya Krishi Vikas Yojana (RKVY)

- RKVY scheme continue during the Twelfth Plan whereby RKVY funding will be routed into three components, viz. production growth, infrastructure & assets, & sub-schemes and flexi-fund.

- The proposed allocation during 2015-16 is Rs 18,000 crore.

- States are at liberty to spend up to 100 per cent of total outlay in the infrastructure and asset creation component.

The National Food Security Mission

- New target of additional production of 25 million tonnes of foodgrains by the end of the Twelfth Five Year Plan (2016-17) comprising of

- 10 million tonnes rice.

- 8 million tonnes wheat.

- 4 million tonnes pulses.

- 3 million tonnes coarse cereals .

- In addition to rice, wheat and pulses, crops like coarse cereals and commercial crops (sugarcane, cotton, and jute) have been included since 2014-15.

- Promotion of farmer producer organizations (FPOs), value addition, dal mill, and assistance for custom hiring charges have also been undertaken under the Mission.

- The pulses component has been allocated fifty per cent of total funds under the NFSM in order to increase their production.

- To promote the use of bio-fertilizers, subsidy on bio-fertilizer has also been enhanced from Rs 100 per ha to Rs 300 per ha.

Mission for Integrated Development of Horticulture (MIDH)

With effect from 2014-15, the Mission for Integrated Development of Horticulture (MIDH) has been operationalized by bringing all ongoing schemes on horticulture under a single umbrella.

- Production and distribution of quality planting material, productivity improvement measures through protected cultivation, use of micro-irrigation, adoption of integrated pest management and integrated nutrient management along with creation of infrastructure for post-harvest management and marketing are focus areas of the MIDH.

SUSTAINABILITY AND ADAPTABILITY

The following initiatives announced in Budget 2014- 15 have brought the issue of sustainability and climate adaptation to the forefront:

- The Pradhan Mantri Krishi Sinchayee Yojana with allocation of Rs 1000 crore.

- Neeranchal, a new programme with an initial outlay of Rs 2142 crore in 2014 to give additional impetus to watershed development in the country,

- The National Adaptation Fund for Climate Change, with an initial sum of Rs 100 crore.

- A scheme to provide, in mission mode, a soil health card to every farmer, with an allocation of Rs 100 crore.

- An additional amount of Rs 56 crore has been allocated to set up 100 mobile soil-testing laboratories across the country.

ALLIED SECTORS: ANIMAL HUSBANDRY, DAIRYING, AND FISHERIES

Indian agricultural system is predominantly a mixed crop-livestock farming system, with the livestock segment supplementing farm incomes by providing employment, draught animals, and manure.

Dairy

- India ranks first in milk production, accounting for 17 per cent of world production.

- The average year- on-year growth rate of milk, at 4.18 per cent vis- à-vis the world average of 2.2 per cent, shows sustained growth in availability of milk and milk products for the growing population.

Poultry

- In the poultry segment, the government’s focus is on strengthening the family poultry system, which addresses livelihood issues.

- Egg production was around 73.89 billion in 2013-14, while poultry meat production was estimated at 2.68 MT.

Fisheries

- Fisheries constitute about 1 per cent of the GDP of the country and 4.75 per cent of agriculture GDP.

- The total fish production during 2013-14 was 9.58 MT, an increase of 5.96 per cent over 2012-13.

National Livestock Mission

The National Livestock Mission has been launched in 2014-15 with an approved outlay of Rs 2,800 crore during the Twelfth Plan. This Mission is focusing on:-

- improving availability of quality feed and fodder,

- risk coverage,

- effective extension,

- improved flow of credit, and

- organization of livestock farmers / rearers.

Given the high contribution of protein items in inflation, the growth rate of this sector has to match the rising demand reflected in increasing share of these items in consumption expenditure.